Welcome to our quarterly investment overview

As promised, I am providing you with our quarterly update. The emphasis isn’t anchored too much on what has happened, more on how we believe monetary policy, economies and markets may unfold.

Predictions are not our bag and those investment houses that fell into this trap were generally proved to be wide of the mark last year. For us at Blue Sky, it’s understanding the dynamics, working out how to respond and choosing, wherever possible, the right asset classes at the right stage of the economic cycle.

This Quarterly Update had been written with the backdrop of falling inflation and falling mortgage rates in mind. Despite deteriorating geopolitical news, investment market sentiment has become more upbeat. But we are acutely aware that deteriorating company earnings may dampen investor sentiment in the first half of 2024, and we are also cognisant of the potential for nasty short sharp shocks arising from conflicts.

It’s interesting how quickly sentiment can change, and this is highlighted with the latest forecasts on the housing market from property agent Knight Frank. It was only in October last year that they were predicting property prices would fall by 4%. Just three months on they are now forecasting that property prices in the UK will rise by 3%. All due to a significant drop in mortgage rates.

Conversely, investment markets were buoyed by the prospects of aggressive interest rate cuts in late October last year, but this week, both equities and bond prices have gone into reverse on weaker sentiments from central banks.

In 2023, money market funds were the only asset class to receive net inflows. Equity funds had a total of £18 billion outflows. Yet, it was a year in which many equity indices performed positively. An article in Investment Week commenting on Morningstar’s latest UK Fund flows, reported that there wasn’t a single month of net inflows. Fixed Income Funds also saw outflows of £7.8 billion for the year.

Business confidence

Concerns about business investment persist with hopes resting on pre-election giveaways and an increase in real disposable income. Many companies have chosen to pay down debt rather than invest into their business with there being so much uncertainty about refinancing.

Of late, there has been a clamour from company executives in the UK urging the Bank of England (BoE) to start cutting rates to avoid a recession. Bloomberg report that mounting fears over an economic slowdown, drove the Institute of Directors’ Economic Confidence Index (ECI) to a four-month low in December. The ECI measures UK company Directors’ optimism regarding the economy for the next 12 months.

Source: JPMorgan Asset Management

Recession or soft landing?

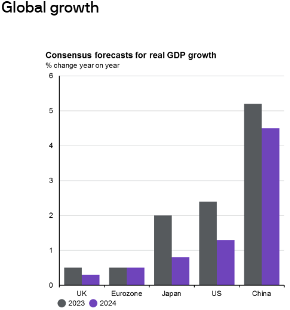

The first week of the new year unveiled a mixed outlook for the UK economy as surveys of economists published in the Financial Times and The Times portrayed a consensus on sluggish growth in 2024, teetering on the edge of a technical recession. Analysts anticipate gross domestic product (GDP) growth between 0% and 1%, with a looming general election adding a layer of uncertainty. The Bank of England, while expected to cut interest rates, is likely to tread cautiously as the battle against inflation continues.

Late cycle challenges

A whole raft of reports and data have surfaced at the start of this year. Some reporting the fastest decline in prices in more than a decade and some championing increased consumer demand on the back of mortgage rates falling. As mentioned at the beginning of this update, Knight Frank have done an about turn on their property price expectations.

However, the unexpected rise in UK inflation, albeit of only 0.1%, is expected to dampen lenders’ enthusiasm to bring down mortgage rates. The Office for National Statistics report that in the 12 months to December 2023, UK rental prices rose by 6.2%. This is blamed on a shortage in property supply, along with high interest rates, and the difficulties of getting mortgages.

Francis Chua from Legal & General Investment Management said they expect Corporate Earnings to come under further pressure. They proved very resilient in 2023 but the lagged effect of aggressive rate rises, and the difficulties of some companies refinancing, may impact profitability.

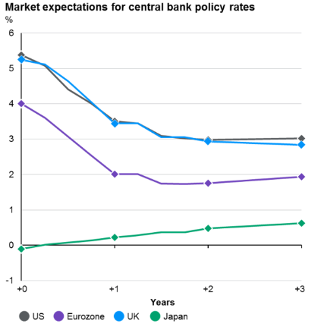

The path for interest rates

With inflation rising to 4% in the UK, suddenly the brakes have been put on the more optimistic expectations of dramatic interest rate cuts. Central banks this week, across the developed world, have warned that there is unlikely to be an immediate rate cut, disappointing investment markets. Events in the Middle East haven’t helped matters with the price of goods expected to increase due to ships avoiding the Red Sea.

There was a good article in City A.M. this week quoting various experts on what the surprised inflation data means to the likely pathway for lower interest rates.

Yael Selfin, Chief Economist at KPMG UK, stated that the slight rise in inflation shouldn’t be a cause for concern, as of yet. She went onto say “the expected fall in the energy price cap in April could see inflation returning to target by Spring. Nevertheless, disruptions in the Red Sea impacting supply chains, could cause further increases in goods prices adding uncertainty to the economic outlook.”

She added that the “overall improvement in the outlook for inflation, coupled with the slowdown in the domestic economy, will likely put the Bank of England in a position to begin cutting interest rates from the second half of the year, potentially lowering rates by 100 basis points in 2024.”

Meanwhile, Ruth Gregory, deputy UK economist at Capital Economics, said the rise in inflation may have been “disappointing”, but “we still expect favourable base effects and a fall in utility prices to drag CPI inflation below the 2.0% target by April, leaving the Bank of England in a position to cut interest rates by June.”

Previously, the markets had anticipated a rate cut in May. Roger Barker, Director of Policy at the Institute of Directors, explained that “inflation in the economy is still broadly moving in the right direction. We still believe that the Bank of England should consider a cut to interest rates sooner rather than later in order to provide a boost to depressed levels of business confidence.”

Carsten Jung, Senior Economist at the Institute for Public Policy Research added that “even though inflation inched up slightly, it is coming down more quickly than many predicted just a month ago. It should be remembered that the main reason for the rise in inflation were alcohol and food. This week’s rise in inflation may be a blip for the UK economy, but it’s important not to overstate its importance. It was a relatively modest increase in price rises, driven by some volatile items. Although it is a good counterweight to the complacency which had been growing in the market, it does not require any significant change in the direction of policy from the Bank of England”.

Source: JPMorgan Asset Management

Good news for Bonds

After the demise of recent years, bonds have had the much-expected resurgence, although the fixed rate assets have responded negatively to the latest inflation data and the interest rate rhetoric. Given the comments above re the direction of travel on inflation, bonds look an attractive proposition. Only this week, Spain attracted the largest ever order book for a sovereign bond, capping a series of ‘blockbuster’ Eurozone debt sales at the start of 2024 (ft.com). The bumper demand for Spanish bonds comes after debt sales in Belgium and Italy on Tuesday also attracted frenzied orders. Investors have queued up to buy eurozone sovereign debt early this year despite a powerful rally in the final two months of 2023 that pulled yields sharply lower. Bankers said the prospect of a series of interest rate cuts by the European Central Bank (ECB) had encouraged big orders from fund managers betting on further gains. The ECB’s benchmark interest rate is expected to fall to 2.75% by the end of 2024 from 4% currently.

JPMorgan’s Global Market Strategist, Max McKechnie believes bonds offer real value, although one has to be selective in the type of exposure. Core fixed income looks very attractive.

Investment sentiment

I’ll expand more on what our investment partners say later but I thought I would set the tone with the broad view from Church House Investments, which I thought nicely sums up where we are.

“As we move into 2024, we have the new dimension of elections to consider. Starting with Taiwan and ending with the long run-in to the US Presidential Election and a possible wild card of a UK election if PM Sunak decides to go early, there is plenty of scope for grand-standing and consequent market volatility. Most economists appear to have shifted from the expectation of an imminent recession last year to a belief in a ‘soft landing’ this year. If the Federal Reserve does achieve a soft landing one year after their yield curve first inverted, it will be a first and impressive. Going back over the eight US recessions since the late 1960s, the economy has fallen into recession around one year after the first negative yield curve on each occasion. We must recall too that a couple of years ago, central banks looked flat-footed and humiliated as the inflation genie escaped and the long shadow of the 1970s loomed. How they react now is all important, but we should not be surprised if they wait too long before cutting rates.”

Francis Chua, a Fund Manager from LGIM commented on how their outlook has become more positive than it was at the beginning of 2023. This is simply because they believe there is a higher probability of a softer landing for economies. The risks haven’t gone away but they have weakened. They are also seeing evidence that the Federal Reserve (Fed) is looking to support markets on signs of weakness. However, the US economy has largely been remarkably resilient.

JPMorgan’s Global Market Strategist, Max McKechnie said to me that they are still quite cautious in their outlook. Their view is that this ‘last leg’ may take a bit longer than expected.

What is the outlook for equities?

The outlook is much improved as we see the slowdown in inflation and a cut in interest rates, but we may see a demarcation between those companies which have strong balance sheets and those that don’t. Growth orientated companies should benefit in the second part of 2024 as capital becomes cheaper, although global growth is still expected to be relatively sluggish.

In our outlook, we must consider the wider issues of geopolitics. Whilst this is impossible to predict, it does naturally bring anxiety on many levels. Whilst we have always seen conflicts around the world, there is no doubt the press coverage has ramped up the feelings of uncertainty, particularly around the rhetoric of World War III being just around the corner, now that Iran is actively seeking to destabilise the region.

I came across a graph the other day (too complicated to include) but it was interesting because it showed how investment markets tend to react when wars break out. On most occasions, stock markets rise because they know what they are dealing with and can then make a rationale around the situation. Not that I’m saying conflict is a good thing; far from it, but I’m just raising the point that market wise, it may not have the effect one thinks. We recognise however, that there does seem a plethora of conflicts involving a whole raft of nations, including the major powers.

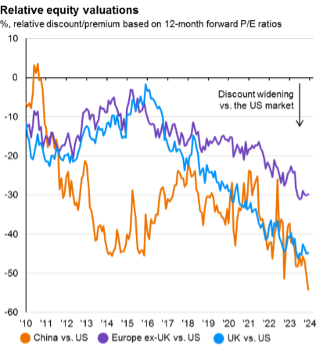

JPMorgan’s Global Market Strategist, Max McKechnie commented that that the outlook for equities is not as good as it is for bonds. Similarly, Ben Palmer of LGT Wealth Management agreed and has concerns for some growth assets with low growth predicted. LGT are concerned about the concentration risks of the ‘magnificent seven’ technology stocks in the US. The Nasdaq this week has attained an all-time high. The US markets were the success story last year but when one strips out the influence of these technology stocks the performance looks somewhat different.

Below is a graph which shows relative equity valuations for China, the UK and Europe versus the US which suggests there are opportunities out there whilst also reinforcing the strength of the US market.

Source: JPMorgan Asset Management

Possible election impacts

We have made the point before that circa 50% of the world’s population is going to the polls this year. As a result, there is bound to be quite a bit of turbulence depending upon their influence on the world stage. The biggest being the US elections.

I like the way LGT Wealth Management position their thoughts:

Once again, the US Presidential election is set to be one of the most hectic, uncertain elections of our time. Following former President Trump’s resounding win in the Iowa caucuses, it appears the US election is shaping up to be a rematch between President Joe Biden and Trump. However, given both candidates are largely unpopular, the likelihood of a third candidate entering the running is high. It’s important to emphasise that despite the market noise, the S&P 500 has not declined in a Presidential re-election year since 1940!

This is because in a re-election year (like we are in today), the President running for re-election has access to an extensive toolkit to ensure the economy remains robust, allowing them to best position themselves for re-election. Since 1950, every President who had a recession within two years before their re-lection has lost. Conversely, every President who avoided recession two years prior to their re-election has gone onto win. Biden it would appear has an advantage but who knows what may happen in US politics!

Enticing themes and opportunities

JPMorgan’s Global Market Strategist, Max McKechnie highlighted that if you are drawn to equities the UK looks relatively cheap on most metrics, assuming a medium to long-term view. He commented that the FTSE 100 plays into the themes unfolding this year, of high-quality firms delivering a reliable income stream. The best value is in the smaller cap space, but one has to be guarded because they are cheap for a reason and as we all know, they can be very volatile.

China is also screamingly cheap. Max spoke about the challenges in this economy and spent some time discussing how China has moved to a consumer economy. As we all know the surge in property builds and prices is creating a significant drag on the nation. He said “how do you get consumers who are concerned about their wealth to go and spend”. Max, like us at Blue Sky, prefers a broader far eastern exposure as countries in the region are really benefitting from China’s difficulties. South Korea and Taiwan come to mind as specialist in semi-conductors.

Max believes the US looks toppy and they are concerned about the concentration risks of the large 7 tech stocks.

I spoke with Max about ESG (Environmental, Social, Governance) and in their eyes Europe are heading the drive for such initiatives, whereas the US are near the bottom of the pile despite their initiatives in recent years. They are very positive in the ESG space and it feeds into many themes.

Large corporates on the whole, are doing a great job but we need more heavy lifting from governments. Ben Palmer from LGT Wealth believes that politics and policy around ESG will help dictate the pace of change. “It’s a shame that the messaging from some governments has been so weak at a time when many corporates are making huge strides” he said. They have embedded structural and economic ESG regimes which are resulting in huge costs savings, alongside reducing the amount of energy used and being able to sell their waste.

LGT also are very interested in the healthcare transition and diagnostics. This is opposed to the typical pharma companies associated with health funds. Ben also positively commented on AI and its place in the health sector.

Francis Chua from LGIM stated that they like fixed income and credit (bonds) but prefer a broader global remit due to political and specific economic risks. They also like emerging market debt, particularly if the dollar weakens. Max from JPMorgan believes the way to play this sector is in local currency.

LGIM are more guarded about the far east because of a significant downgrade in China’s earnings. If the economic story holds up, they like UK and European small caps, but this isn’t a focus at the moment as they are still guarded on the economy. Infrastructure now looks appealing with huge discounts on the underlying property assets, with the upside of this asset not being dictated by consumer confidence, with the added benefit of inflation linked earnings. Like us at Blue Sky, they believe that in the immediate term, bonds offer more security but once interest rates start to fall, we will no doubt pick up some infrastructure again.

Staying on the subject of infrastructure, I spoke to Mike Parsons who is the Head of Distribution at Foresight, a renowned specialist who we have worked closely with. He spoke about how infrastructure can be viewed as economically insensitive due to government contracts and inflation linking. Mike agreed that the sweet spot for infrastructure will be if inflation comes down, interest rates fall, but they remain higher than was the case in pre Covid times. Mike also communicated that if bond volatility subsides that is normally good for infrastructure.

I asked Francis for his thoughts on commodities and natural resources and we both agreed that typically the best time to go into these assets is at the end of a recession or slowdown. The feeling being that now is too early with sluggish global growth.

LGT Wealth are focused on those companies with strong resilient balance sheets, regardless of immediate growth prospects. This is more prudent then ever with many companies having to refinance in a difficult credit market.

Summary

As you can imagine, there is always a wide spectrum of opinions but what was evident in this round of discussions is how aligned various investment houses are on their thoughts. Cautiously optimistic, is how I would describe their outlook. If it wasn’t for the uncertainty of geopolitical issues, be it around conflicts and/or elections, the tone would be more upbeat, although there are still words of caution around corporate earnings in some quarters. The beacon of light is undoubtedly bonds with inflation expected to continue falling. In October, for our in-house portfolios we picked up bonds which have served us well. The bond market is much bigger than the equity market and is more complex in many ways and therefore we lean heavily on our investment partners for their research and expertise.

Sentiment about a recession has improved and the expectation now is for a soft landing but sluggish growth across economies. Interest rates will begin coming down this year and don’t be surprised if inflation falls more quickly than is being forecast. Change is a constant as this graph of the FTSE 100 shows over the last 6 months (source ft.com). I think it’s fair to say there has been quite a lot of volatility! The overall trend from the end of summer has been upwards.

Our view at Blue Sky, is despite the short-term fluctuations in sentiment, the good news is that bonds are ‘back in the ring’ which should serve to provide more ballast and stability to portfolios as inflation and interest rates fall.

I hope you found this overview useful. In many ways, it just pulls together what I’ve been saying in recent weeks but if you want more detail, then please ask.

Have a great weekend.

Gary and the Blue Sky Investment Team

Risk warning

Please Note: This communication should not be read as giving specific advice regarding your personal circumstances. This would only be given following detailed assessment of your individual needs. The value of investments may fall as well as rise; you may get back less than invested. Past performance is not necessarily a guide to future returns.