What our investment partners say

As promised, this week I’m providing an overview of what some our investment partners (LGT Wealth, JPMorgan, LGIM and Foresight) think about the outlook for markets, along with other investment analysts. This is one of those occasions when you’ll need to make a bit of time and sit down with a good cup of coffee,or something else you are partial too.

We conducted our quarterly assessment by engaging with respective fund managers and representatives of each company to understand their thoughts. We receive frequent updates from them all and benefit from their huge amount of research on an ongoing basis. However, it’s always good to reflect on what has happened, as in many ways this informs what is likely in the foreseeable future.

Investing is clearly not an exact science but despite frequent setbacks we are seeing a positive direction of travel for both equities and bonds since the lows in October of last year.

A quick look at what’s happened in Quarter 1 of 2023

Bonds and equities were broadly in positive territory for the first quarter of this year but it hasn’t been plain sailing!

Sanjay Rijhsinghani, the Chief Investment Officer of LGT Wealth summed the quarter up nicely:

Sanjay Rijhsinghani, the Chief Investment Officer of LGT Wealth summed the quarter up nicely:

- The early part of the year saw growth moderating which excited the markets as it was believed we were coming to the end of the interest rate cycle.

- Then hopes were dashed somewhat in February due to data demonstrating that economies appeared more resilient than expected, helped by lower energy prices.

- The strong opening of China was a positive for markets, giving the likes of Europe a significant trading boost.

- Then the ‘mini’ banking crisis placed pressure on bank lending which is believed to have a created an impact equivalent to an interest rate rise of between 1-1.5%.

- Central authorities reacted quickly though to bring calm and stability.

What is the general view around equity markets?

All investment houses echoed our view that there is a two-speed recovery unfolding, the Far East and Emerging Markets and then the developed world. As Hugh Gimber, a Global Market Strategist at JPMorgan highlighted, it’s also important to differentiate between the UK, Europe and the US because although they are in similar parts of the economic cycle, they have their own unique circumstances.

UK

The UK is frequently seen as the poor relation in economic terms to other developed nations but the dire forecasts from the International Monetary Fund (IMF) and the Bank of England (BoE) haven’t materialised and UK markets performed more strongly than anticipated. It’s true to say that many forecasts have been wide of the mark from multiple respected sources, not just in the UK but with respect to the global economy. It just goes to show what uncertain times we live in.

This week, the IMF upgraded its outlook for the UK economy, saying it now believes the UK is on track to contract by only 0.3% this year (half the 0.6% decline the IMF forecasted in January) before expanding by 1% in 2024.

It is still expected that the UK will be the worst-performing developed economy, alongside Germany, which is likely to dip its toe in to negative growth, albeit briefly.

Of course, the data can be spun into all manner of headlines. Another way of looking at this is to note that the IMF forecast has upgraded the UK by more than any other G7 country.

Certainly, the government will spin the positives. Jeremy Hunt has already signalled that a UK election may be held as early as Spring 2024 according to Bloomberg, a time when they hope the economy will have turned the corner. The chancellor told Bloomberg that “all official forecasters expect Britain to be growing in a year’s time, and for inflation to be under control at around 3%”.

The IMF are similarly minded, and it points out that interest rates are likely to return towards pre-pandemic levels once inflation is tamed due to poor growth in the developed world. Not quite the sentiment that is followed by our various investment partners. Sanjay at LGT Wealth believes we should get used to higher interest rates, albeit, down from these elevated levels and the same goes for inflation which may prove to be elevated above the BoE’s target of 2% for some time.

A significant fall in interest rates would be welcome to mortgage holders but it must be borne in mind that this suggestion by the IMF is based on a gloomy outlook of low productivity and an ageing population.

After narrowly avoiding recession in 2022, Britain’s economy has shown some signs of resilience in early 2023. The BoE says it expects slight growth in the second quarter after a small contraction in the first three months of the year.

Rishi Sunak and Jeremy Hunt are under pressure to get Britain’s economy growing more quickly before a possible election next year, but so far, they have defied pressure from within the Conservative Party to cut taxes, saying they are focused primarily on lowering inflation.

The IMF forecast Britain’s inflation would average 6.8% in 2023, down from 9.1% in 2022 but still way above the BoE’s 2% target and the highest among the G7 countries. Time will inform us as to who is right!

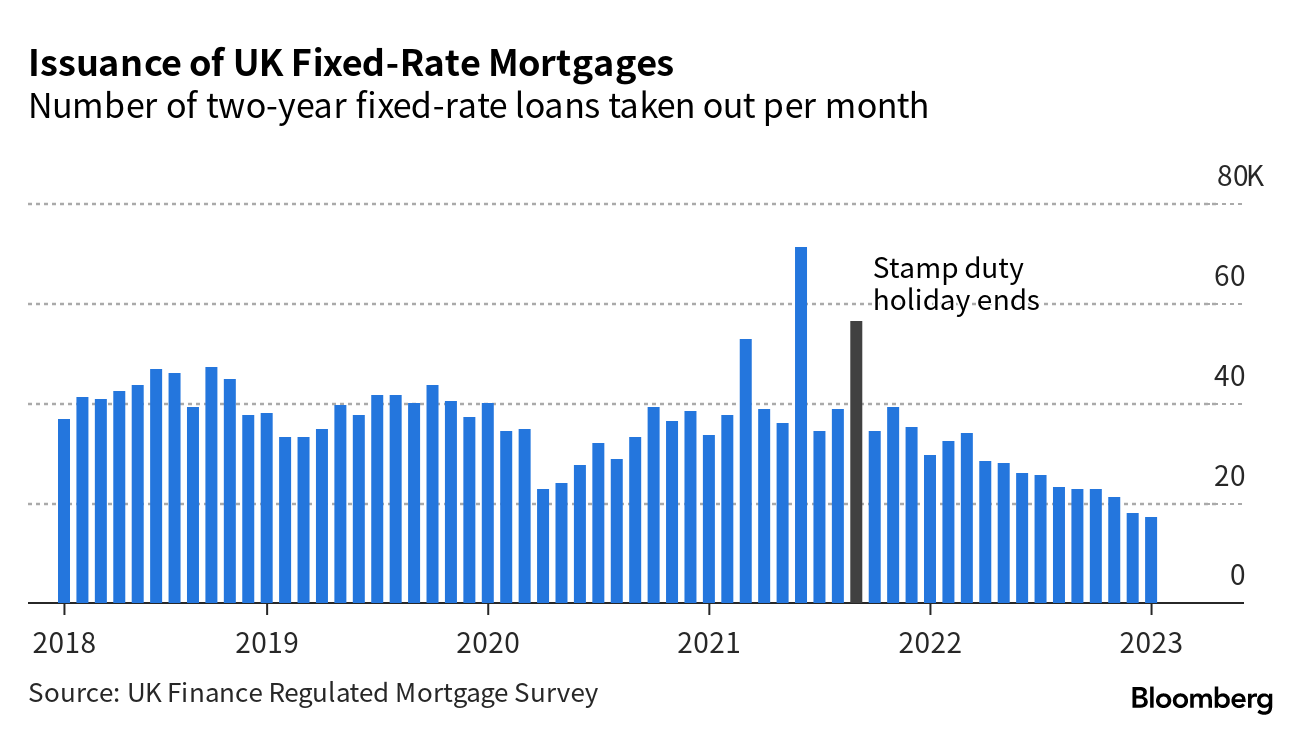

The here and now for mortgage holders

According to UK Finance, 56,220 two-year fixed-rate mortgages are expiring in September. As Bloomberg reports, this comes on the back of a flurry of sales in September 2021 before a stamp duty holiday ended. The average two-year fixed-rate mortgage was 5.32% on 11th April. The two-year tracker deal was 5.05% this week, meaning cheaper monthly payments for variable loan holders.

However, there may well be a silver lining, despite these fixed rates coming to an end. Most borrowers will have paid off a chunk of capital from their mortgage via a repayment loan since March 2021. Furthermore, UK house prices have grown by more than 11% in the last two years. This should help borrowers in that they will have a lower loan-to-value ratio than when they secured their mortgage.

Europe

Europe has benefitted hugely from increased optimism. European equity prices were suggesting dreadful times for the Eurozone, especially with the energy crisis. The reality was not as bad as feared and European equities have risen strongly as a result.

Europe sourced alternative energy supplies, particularly from the US and this, along with a mild winter, helped the resilience of the Eurozone.

The IMF suggests that low inflation and weak growth will trigger central banks to slash interest rates. This is most likely to impact the UK, Germany and France.

Yet, it would be folly to treat the Eurozone as one entity, just as it would be to group the developed countries together. There are a lot of strong, well-run companies in Europe and we should not underestimate the desire of the authorities to elevate Europe’s positioning with stimulus and incentives down the line. We have already seen this with regards to net zero strategies.

After growing 3.5% last year, the EU is viewed as growing 0.8% and 1.4% according to an article published in Investment Week.

US

“Will they, won’t they increase interest rates” – this is still the mantra dominating the thoughts of many analysts.

The meeting minutes of the Monetary Committee suggest that another rate hike is required in the US, this is despite warnings from some quarters, of an increased likelihood of a recession. However, their expectations of how high they may have to raise rates has been lowered, indicating that there may even be a pause in the coming months.

Helping the cause was the announcement this week of US inflation figures. From February, US inflation fell by 1%, from 6% to 5%. The markets were expecting 5.1% and have responded positively to the news.

Hugh Gimber from JPMorgan noted that following the banking crisis, the case for the Federal Reserve to pause interest rates is becoming more compelling. He commented “for the past year, the Fed has been solely focused on tackling inflation. With increasing evidence that the battle is now being won, policymakers can start to factor the growth outlook back into their decision making as well”.

Hugh Gimber from JPMorgan noted that following the banking crisis, the case for the Federal Reserve to pause interest rates is becoming more compelling. He commented “for the past year, the Fed has been solely focused on tackling inflation. With increasing evidence that the battle is now being won, policymakers can start to factor the growth outlook back into their decision making as well”.

Hugh also went on to say how helpful this next phase will be in assisting multi asset portfolios because it heralds the return of high-quality fixed income (bonds) as a diversifier against recession risks.

Asia and Emerging Markets

Despite a mixture of improved data, the general forecasts from the IMF are quite gloomy, although it’s important to point out that there are various outcomes for differing scenarios. Their view on emerging markets and developing economies are like light and shade with them expecting strong growth in these domains.

They forecast emerging markets to grow by 3.9% this year, after a growth of 4% last year and 4.2% next year. China’s forecast came in at 5.2% and 4.5%, with India leading the way at 5.9% and 6.3%.

The superior growth rates make these regions attractive. Emerging markets and developing economies don’t have the same set of problems as developed markets.

All our investment strategist were aligned on the opportunities unfolding within emerging countries.

Global

Overall, the IMF downgraded its forecast for global growth by a small margin of 0.1% from its 2.9% projection in January, lower than the 3.4% seen last year, with a slight recovery next year to 3%. However, they believe there is a 25% chance that global growth will fall below 2% for the first time since the 2008-09 global financial crisis.

The IMF’s Chief Economist, Pierre-Olivier Gourinchas, said the global economy was at risk of a hard landing, pointing to governments and central banks being behind the curve on getting the inflation genie back in the bottle whilst avoiding slamming the brakes on growth and employment. He said “we are entering a perilous phase during which economic growth remains low by historical standards and financial risks have risen, yet inflation has not yet decisively turned the corner”.

The IMF’s Chief Economist, Pierre-Olivier Gourinchas, said the global economy was at risk of a hard landing, pointing to governments and central banks being behind the curve on getting the inflation genie back in the bottle whilst avoiding slamming the brakes on growth and employment. He said “we are entering a perilous phase during which economic growth remains low by historical standards and financial risks have risen, yet inflation has not yet decisively turned the corner”.

Advanced economies are now projected to grow by 1.3% this year and 1.4% in 2024. Within the G7, the US leads the way with an expansion of 1.6% in 2023 and 1.1% in 2024. Canada is eyed at 1.5% for both this year and next, with Japan following with estimates of 1.3% and 1% respectively.

The IMF also trimmed its worldwide growth outlook for this year, warning that stubbornly high inflation and any further chaos in the banking system could slash output to near recession levels.

“With the recent increase in financial market volatility, the fog around the world economic outlook has thickened,” Pierre-Olivier at the IMF said. “Uncertainty is high, and the balance of risks has shifted firmly to the downside so long as the financial sector remains unsettled.

“Inflation is much stickier than anticipated even a few months ago. While global inflation has declined, that reflects mostly the sharp reversal in energy and food prices”.

Certainly, this is the view of Francis Chua, a fund manager at Legal and General Investment Management (LGIM) who stated that they are more underweight in equities than they were a couple of months ago.

Certainly, this is the view of Francis Chua, a fund manager at Legal and General Investment Management (LGIM) who stated that they are more underweight in equities than they were a couple of months ago.

As reported in the Telegraph this week, Barclays stated that the banking crisis has shaken US and Europe and has caused investors to flee from equities. This may have been the case initially but the recent recovery in equity prices suggest that there are also opportunists taking advantage of pull-backs in the market.

The analysts at Barclays are forecasting that $1.5 trillion (£1.2 trillion) will be invested in low risk money market funds over the next year, rather than in stock markets or other investments. The suggestion is that this will likely hinder growth by making it harder for companies to raise money.

The amount of money parked at all so-called money-market funds climbed to a fresh record last month. Their cash pile jumped by roughly $304 billion in three weeks, bringing total assets to $5.2 trillion as of 29th March, according to data from the Investment Company Institute.

Are bonds still off limits?

No, quite the opposite. There is a lot more appetite for bonds as inflation falls. The focus from all our investment partners was on government bonds as opposed to Corporate bonds because of endemic economic risks. There was also an emphasis on having a global spread of Government bonds to avoid any specific Central Bank being wrongfooted or making strategic mistakes.

During 2022 the emphasis was on short duration assets to avoid an over exposure to credit. We are now seeing more of an appetite for longer duration assets now that there is more stability, particularly in the UK.

Sanjay from LGT Wealth commented that it was good to see traditional safe haven assets behaving as safe haven assets once again, after the turmoil of last year.

Infrastructure promised but struggled

Up until September, infrastructure was one of the few asset classes in positive territory but more aggressive inflation numbers arose and on our shores we had a new Prime Minister which resulted in short-term economic chaos, elevating inflation numbers to even higher levels.

Infrastructure suffered in a similar way to bonds with a dislike for longer duration earnings, in favour of shorter exposures, even though largely these earnings were predictable and were mainly backed by governments. With Infrastructure benefiting from index linked contracts one could be forgiven for thinking that such assets would be a beneficiary. However, such aggressive inflation caused a great deal of fear and turmoil. One only has to look at the UK government and the resultant turmoil in September and October of last year to understand why. This crisis (Liz Truss) meant that the cavalry, in the form of the BoE, had to ride to the rescue.

The outlook appears much better for infrastructure. As an asset class it likes some reasonable level of inflation and if the numbers are ‘sticky’ then this should be good news. One also has to bear in mind that the earnings for indexation take some time to feed through into earnings.

Sustainability

Phoebe Stone, the Head of Sustainability at LGT Wealth, who is always a pleasure to listen too, reinforced what a bad year 2022 was for the Sustainable space. It was trumped in many ways by the move out of growth orientated companies into more traditional value-based companies. We also saw huge swathes of money exiting ESG assets (Environmental, Social and Governance) towards contrarian oil, gas and mining companies.

Phoebe Stone, the Head of Sustainability at LGT Wealth, who is always a pleasure to listen too, reinforced what a bad year 2022 was for the Sustainable space. It was trumped in many ways by the move out of growth orientated companies into more traditional value-based companies. We also saw huge swathes of money exiting ESG assets (Environmental, Social and Governance) towards contrarian oil, gas and mining companies.

The last six months have seen a marked improvement in the performance of Sustainable orientated assets, outperforming many of their mainstream counterparts.

There is no doubt in Phoebe’s mind that the politicisation of ESG clouded the view of the good work that has been going on. Many exciting opportunities are unfolding.

“2023 started off strong for Sustainable funds, helped by increasing evidence from lawmakers of the importance of Sustainability in terms of the regulatory regime as the lack of clarity around Sustainability was deemed a risk factor.”

Janet Yellen, the US Treasury Secretary stated that the US is not doing enough and pointed to the economic and financial implications of not stepping up. Phoebe believes this is a powerful reminder to investors and markets that climate risks are also a financial risk, should change not be embraced.

Add in the ground breaking policy legislation in Europe and its clear to see that Sustainability is front and central of business decisions, certainly amongst larger corporates. The initiative by Europe has been introduced in response to the pioneering legislation in the US whereby they give tax credits, amounting to billions of dollars, to companies relocating some of their supply chain into the green transition space.

This involves energy efficiency, the use of renewable energy and greener technology etc. It has encouraged companies to relocate their assembly plants. Volkswagen have identified that it would save them $11 billion to their tax ledger over the next five years. As a result, Volkswagen have committed to $2 billion to electric vehicle assembly plants.

Amazingly, Europe responded by matching any such tax credits which keeps European companies competitive. The UK government will brief us in the autumn as to how they will respond.

Europe is also seeking to speed up the administration and resultant grants to companies with a view of mobilising the sector. It’s looking to protect their supply chains and be less reliant on other countries, particularly in unstable parts of the world. They are seeking to achieve a higher percentage of processing and mineral extraction in Europe, whilst also wanting to recycle 40% of its requirements.

Phoebe says this is one of the biggest investment opportunities but also is one of the biggest risks for companies not responding to change.

What can we expect?

Earnings season kicks off

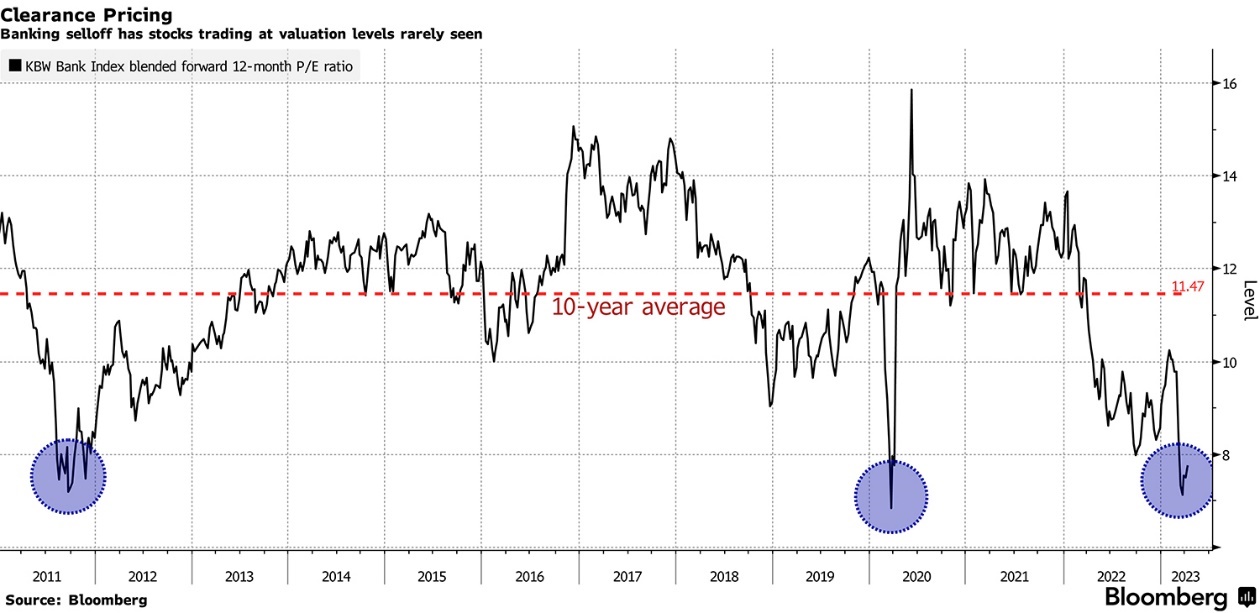

Today’s bank earnings come as industry valuations are looking cheap.

The KBW Bank Index, which fell 25% in March amid the US regional lender turmoil, is trading at 7.8 times earnings, according to Bloomberg. The index’s Price Earnings Ratio (PE ratio) has been this low only twice in the last 12 years.

Then there are the broader implications: “Bank earnings typically set the stage for the rest of earnings season plays out”, New Constructs CEO David Trainer said.

Investment Trusts are offering big discounts

The Investment Trust and Funds sector is experiencing the ‘widest discount’ since the global financial crisis, as the turmoil of March took its toll on performance. The sector ended the first quarter of 2023 down 1% after a promising 6% rise in January, an underperformance versus the FTSE All Share, which returned 3%.

According to an article in Investment Week, the average discount for the funds sector widened further in quarter 1 from 13-16%, a level not seen since the 2008 global financial crisis. The sector reached similar levels temporarily, after the mini budget of September 2022 and during the March 2020 sell off.

I mention Investment Trusts as they are a good indicator of sentiment and the level of ‘risk on and risk off’. However, in both September 2022 and March 2020, an entry into equities at these points would have been rewarded.

The question therefore is how much of the uncertainty is baked into prices? A reduction in inflation and a pause in interest rates will be good news for consumers and businesses but what we don’t yet know is the impact on earnings.

A dramatic fall in inflation and subsequently interest rates may appear good news but as the IMF point out, this will only be likely when we have a real gloomy economic climate.

What are the recommended strategies moving forward?

- Active management is key. There is a need to be selective.

- There are a plethora of challenges and therefore diversification is important.

- Bonds are now a more useful asset and offer downside protection.

- They are reducing their allocations to mid-cap in favour of more defensive equities.

- Still have a conviction for quality companies with strong balance sheets, not speculative growth companies. Overleveraged companies will struggle to pay their debt.

- Markets are pricing in three interest rate cuts this year in the US. What if this doesn’t happen?

- Those growth companies they are investing into are with a 3-5 year investment horizon in mind. Some great opportunities appearing.

- They believe their portfolios are well placed for whatever unfolds.

- China and the Far East looks attractive, especially with China opening up and the prospect of the authorities injecting stimulus into the economy.

- It’s important to differentiate between specific developed countries and regions as they have their own set of unique factors.

- They are watching earnings very carefully. Earnings have held up well to date, despite concerns ahead of each quarters’ earnings results.

I had a great chat with Francis Chua, not just about his team Manchester United!

- They have moved to an underweight position in equities and overweight in bonds across their multi-index portfolios.

- They are now more bearish after the banking crisis.

- There is a disconnect between markets and economic news.

- Still believe that earnings will come under pressure. Tighter credit conditions will not help companies who are heavily indebted.

- There are still some concerns over systemic risk due to aggressive interest rate hikes.

- Emerging market debt looks attractive. Central banks in this part of the world raised interest rates earlier than their developed counterparts.

- They see a flow of money from the US into Emerging Markets.

- China has struggled more than anticipated. It will take time to break the habits of two and a half years. However, China’s property crisis has improved significantly.

- The Far East is attractive for its growth, and it is in a different phase of development from its western counterparts.

- Europe offers value, more so than the UK. Has been overlooked and its performance over the last six months has been very encouraging.

- They are underweight in the UK. They see challenging times ahead.

- Banks wise, they see the cost of regulation in the US hampering some of the smaller and mid-sized banks. On the contrary, European banks are well capitalised, with better controls.

- Really like Bonds with 4-5% returns on offer. The focus is on government bonds and not corporate bonds.

- Good to see longer-term gilts becoming desirable which points to less concerns about risk in this space.

- Really like ESG orientated assets with recent momentum in the US and in Europe, especially.

I spoke to Mike Parsons at Foresight, a Business Development Strategist with a good, rounded knowledge and he spoke specifically about Infrastructure, but also the wider markets and economic conditions.

- Markets in the Far East are expected to outperform their western counterparts.

- US Net Zero Reduction Act is good for renewable energy which constitutes a good portion of Foresight’s Infrastructure proposition.

- Real assets like Infrastructure are a good place to be when earnings resilience is uncertain.

- Infrastructure is focused on long dated assets which are becoming more desirable again.

- Infrastructure, whilst being a hedge against inflation, struggled with rapidly rising interest rates. Mike pointed out that also it can take time for the inflation hedge to feed through. Remember most contracts have inflation protection.

- The characteristics of Infrastructure are desirable in this market due to strong balance sheets and strong quality of management.

- There is a note of caution around markets in general about not being over extended.

- Falling, but elevated inflation is good for Infrastructure.

- Infrastructure still has a strong part to play as an alternative asset.

Hugh Gimber was on hand to answer my questions with aplomb as usual.

- They do not see a banking crisis. Large banks are well capitalised. Credit Suisse shares had already tumbled from March 2021. Their problems were there to be seen before the recent crisis.

- They see weaker fundamentals across markets. Weaker confidence creates a drag on growth.

- The UK does not look appealing, particularly around strong wage growth in a weakening economy. Europe doesn’t have the same issues.

- Earnings are a concern with weaker economy.

- Not convinced that a big enough economic shock has happened. They like quality, well capitalised companies.

- They like government bonds as a diversifier against risk. The reset last year has brought opportunity as risk builds in the economy.

- Emerging markets look attractive. Their economic cycle is out of kilter with developed markets and inflation and interest rates are under better control.

- Demographics also favour emerging markets.

- They are seeing money moving from India to China as it offers more value in the short-term.

- Emerging market governance for JPMorgan around ESG has always been important.

- They like Infrastructure but mentioned there is often a time lag for cash-flows to feed through.

- When it comes to Infrastructure, Hugh reinforced that it’s a good hedge over time but interest rates moving around more quickly than the long-dated cash-flows can create difficult trading conditions.

- With regards to equity markets in the developed world the focus is on quality and not speculative growth companies.

Summary

A Blue Peter badge for you if you stayed the course and read through this entire update. Thank you!

Clearly, there is a lot going on and we deemed it important to give you a flavour of what the thinking is in the immediacy and beyond. There are some challenging times but also some great opportunities. With change comes opportunities as identified in the ESG space.

The UK is the poor relation in many ways, but it has already surprised on the upside. The UK looks relatively cheap, but this is reflected in its weaker outlook.

Europe is far more attractive but will have challenges around slower growth, although it doesn’t have some of the embedded challenges of the UK.

The US is seeing some money move to other domains and the recent banking crisis has knocked confidence, yet the S&P 500 index is now higher than before the banking crisis. Slowing down the US economy is going to be quite a challenge!

Emerging markets get the consensus vote with stronger economic growth expected and less monetary shocks anticipated in the system. Who would have thought we would be saying this?

Finally, Bonds are being favoured to head off turmoil which may manifest if corporate earnings disappoint. The appetite is for Government Bonds instead of Corporate Bonds.

As an investment committee, we are evaluating our asset allocations and may well introduce some government Bonds into selected portfolios. The credit squeeze caused by the ‘mini’ banking crisis means we will revisit our domestic holdings in the UK but otherwise, from our preliminary chats, we are comfortable with our positioning.

I’m off for a lie down.

Have a good weekend.

Gary and the Blue Sky Investment Team

Risk warning

Please Note: This communication should not be read as giving specific advice regarding your personal circumstances. This would only be given following detailed assessment of your individual needs. The value of investments may fall as well as rise; you may get back less than invested. Past performance is not necessarily a guide to future returns.