Please find below our Investment Market Update as at 8th April 2022.

Blue Sky Investment Market Update

After a week away in Rome and Florence, it was pleasing to come back to the helm following a week of positive gains for our portfolios. I must say, it was also therapeutic to get away from the avalanche of bad news which seems to be unfolding by the hour.

These weekly market updates are intended to provide an insight and much needed perspective, however, we cannot mask the realities of what we may be facing, both economically and financially. Confusing matters at regular junctures, is how investment markets can respond positively to bad economic and financial news and vice versa. Something Gus adeptly referred to in last week’s update.

Is a recession coming?

Over the last few days, equity markets had been fairly sanguine, but they have weakened slightly as the economic outlook seems to be deteriorating. In many quarters, there has been much talk of a recession coming down the tracks which is hardly surprising with supply chains disrupted, inflation soaring to 40-year highs and interest rate rises aggressively predicted.

So, I thought I would share with you the thoughts of Legal & General Investment Management (LGIM) on the possibilities of a recession following our in-depth quarterly review with them.

Caveats

LGIM suggest that before answering whether recession is coming, we must define ‘recession’ carefully. If we stick with the traditional two consecutive quarters of declining GDP (Gross Domestic Product), from an investment market perspective, this should not be seen as a binary event because the impact on asset prices will hinge on the depth, diffusion and duration of the recession.

Blue Sky: In other words, this does not necessarily mean recession is bad news for all investments.

We also need to consider that as trend growth has declined in a number of countries, meeting our definition of recession becomes easier. For Japan or Italy, a mild contraction in GDP probably will not lead to much of a rise in unemployment or reduction in profits.

Blue Sky: Normally, it is significant movements in GDP which causes a recession but following the pandemic, it won’t take much to tip some countries into recession now.

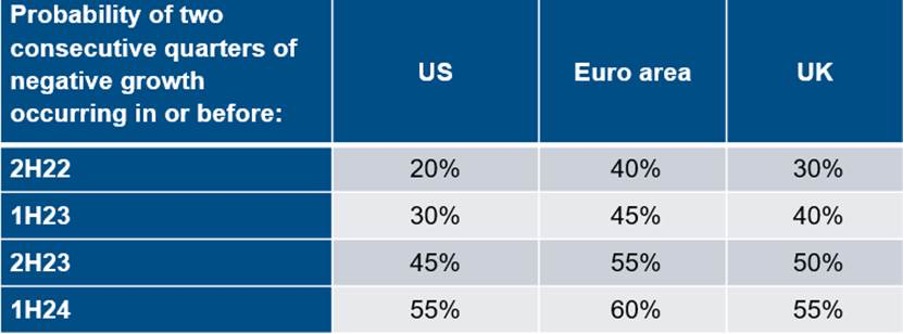

So, what are the chances of a recession?

We are not just talking about the UK here, more the developed economies around the world, with a focus on US, Europe and the UK.

LGIM’s view is:

In the near-term we are much more concerned about recession in the euro area than the US. The euro area is suffering a far greater rise in natural gas prices and squeeze on real labour incomes than in the US which has its own abundant supply. The probability of recession would be even higher in the second half of this year, but there is still scope for a further normalization of services activity assuming concerns around the pandemic fade.

Blue Sky: Translated, this means there is an increasing probability of a recession in Europe unless economic activity picks up as the Covid impact wanes.

For the US, the near-term risk is only marginally higher than a naïve assumption around the chance of recession in any random year. The low unemployment rate raises the risk, but offsetting this is strong near-term momentum helped by the inventory cycle and households with a strong savings buffer. Further out, the probability of recession rises as the Federal Reserve (Fed) is forced to address its persistent inflation problem and raises rates well above its estimate of neutral next year.

Blue Sky: The risks in the US are much lower but much depends on how the Fed responds to the challenges ahead.

Probability

Source: LGIM – periods relate to half years, signifying two consecutive quarters of negative GDP growth.

Blue Sky: Near-term recession risk is elevated in Europe, but for the US there are greater risks in 2023.

How does this impact the investment landscape?

I would like to start this section off by firstly reminding ourselves that change brings opportunities. Secondly, not all assets behave in the same way. For example, since the invasion of Ukraine, our Infrastructure portfolio has risen by over 10%, despite awful news flow and anticipated weaker economic growth.

LGIM’s outlook

Despite the economy slowly and recession risk re-appearing on the radar screen, our immediate reaction is not to sell equities. The historical baseline is that equities deliver strong returns in the late cycle phase and on average, 15% in the last year of a bull market.

In the past, the S&P 500 has peaked on average around six months before a recession. So, our view and that of our economists’ regarding recession probabilities, is that this is a warning sign rather than a sell signal.

While we don’t immediately hit the ‘sell’ button, in this macro environment our approach to risk-taking becomes increasingly tactical and that means sentiment and positioning and how bullish or bearish the market is, are more important drivers of our risk appetite.

The sentiment indicators and our back-testing work are currently sending a fairly neutral signal. While a lot of the bearishness in markets has faded away with the recent rally, there are still no signs that the pendulum has swung all the way back to bullish levels.

Blue Sky: In essence, the sentiment is much improved than it was a few weeks back but it’s difficult to argue that everything looks rosy. The future is uncertain.

A strong resonance with our views

It is interesting to obtain the insights from LGIM about the chances of a recession but aside from this, what LGIM have stated resonates with us here at Blue Sky and feeds in nicely to our previous communications.

We are going to see a significant divergence in asset prices across various sectors and we would argue strongly that it’s never been as important to understand what’s in your portfolio. The days of all equities going up in unison seems a long time ago now. It’s also a challenge to protect portfolios on the downside, as government bonds in western economies, struggle in this higher inflationary environment. This is where alternative assets need to be considered to create ballast but also as a hedge in a high inflationary environment.

Despite the uncertainty, it’s important to understand that we are expecting greater government and business spending which will stimulate economies. More about this next week.

It’s not all uncertain!

Dividend payments are on the rise. As reported in Investment Week, FTSE 100 dividends are set to deliver £114 billion in returns to shareholders in 2022, making it the second-best year on record for returns from the index. Yes, the second-best year on record!

New data from AJ Bell revealed that along with the £32.7 billion in share buybacks already announced, the firm expects FTSE 100 companies to generate £81.2 billion in dividends by the end of the year, as the net profits are expected to hit a record high of £169.7 billion in 2022. However, these estimates even leave nine months of room for additional dividend increases, special dividends and share buybacks to be announced.

Rio Tinto is set to be the FTSE 100’s single biggest dividend payer this year with £7.4 billion, while Persimmon is expected to be the highest-yielding stock at 11.2%.

However, “investors will have to look carefully at the list of the highest-yielding firms, as some of them have a track record of having to cut their dividend payments when times get tough” warned Russ Mould, investment director at AJ Bell.

In total, 97 FTSE 100 firms are expected to pay a dividend in 2022, compared to 91 in 2021 and 85 in 2020.

Summary

A mixed picture for sure, but opportunities will present themselves. We know how quickly things can change!

We are pleased with the asset holdings within our portfolios and feel that our last switch has worked well. Our best performing portfolios since the invasion of Ukraine have been our Infrastructure and Global Themed portfolios, all benefitting from diversification but also are well positioned to benefit from greater investment from governments and businesses alike.

Remember, change brings opportunities.

Have a good weekend.

Gary and the Blue Sky Investment Team

Risk warning

Please Note: This communication should not be read as giving specific advice regarding your personal circumstances. This would only be given following detailed assessment of your individual needs. The value of investments may fall as well as rise; you may get back less than invested. Past performance is not necessarily a guide to future returns.