Please find below our Investment Market Update as at 19th November 2021.

Blue Sky Investment Market Update

Tears for fears!

As many of you will know, this is the name of a band from yesteryear, although I believe they are touring once again next year. One of their iconic songs was entitled ‘Mad World’ and somehow this seems quite appropriate at the moment!

We have heightened border conflicts, the increasing influence by China on global matters, cyber security attacks, concerns over protectionism, trade issues, inadequate supply chains, employment concerns and the lack of overwhelming commitment by all powers to the climate accord. I’m sure in a matter of minutes we could name many, many more issues. Yet amongst all this, equity markets continue to rise!

It just goes to show how important it is to cut through the noise. There are always issues on the world stage, but the real drivers are corporate and economic growth and whether expectations are met or, as is the case at the moment in the US, exceeded. Third quarter figures saw companies maintain profit margins and the accompanying guidance was relatively upbeat.

Inflation… an issue or not?

Despite rising inflation and fears over it remaining elevated, equities continue to rise. The key is that monetary policy hasn’t risen in tandem.

In the US, consumer prices have risen so fast they are close to a 31-year high. Here in the UK, figures announced this week saw inflation reaching a 10-year high. Not helped by electricity costs surging by 18.8% year on year, gas up over 28% and petrol prices at a 9-year high too.

The consensus is that equity prices may remain insulated until the Fed sounds more aggressive, according to many analysts.

Inflation, of course, isn’t necessarily a negative for all equities per se. Certain sectors are viewed as real assets which means they tend to appreciate in an inflationary environment, making some stocks a useful hedge against inflation pressures.

Global dividends also hit a record high

Shareholders were paid record dividends in the third quarter of the year, the highest ever recorded in the three months to September, according to Janus Henderson, as reported in Investment Week.

Dividends are 22% higher than they were over the same period a year ago, supported by rising profits and strong balance sheets. Globally, 90% of companies either raised their dividends or held them steady. The surge in shareholder pay-outs has been driven by bumper dividends from mining companies which have distributed more money in the third quarter alone, than they did in the whole of 2019, before the pandemic. BHP will be the world’s biggest dividend payer in 2021.

The banking sector, not surprisingly, also made a significant contribution, mainly because regulators have lifted restrictions on pay-outs and because adverse loans and defaults have been lower than expected.

Janus Henderson now expects growth of 15.6% on a headline basis, taking 2021 pay-outs to a new record of £1.1 trillion.

Countries which had the steepest cuts in 2020 unsurprisingly saw a rapid recovery. Australia (mining) and the UK (banking) were the biggest beneficiaries. Europe, parts of Asia and emerging markets also saw large increases. Those parts of the world, like Japan and the US, which didn’t see drastic cuts to dividends naturally showed less growth than the global average. Nevertheless, US company dividends rose by a tenth to a new third quarter record. It also appears that Chinese companies are on track to deliver record pay-outs in 2021.

Not bad for a ‘Mad World’!

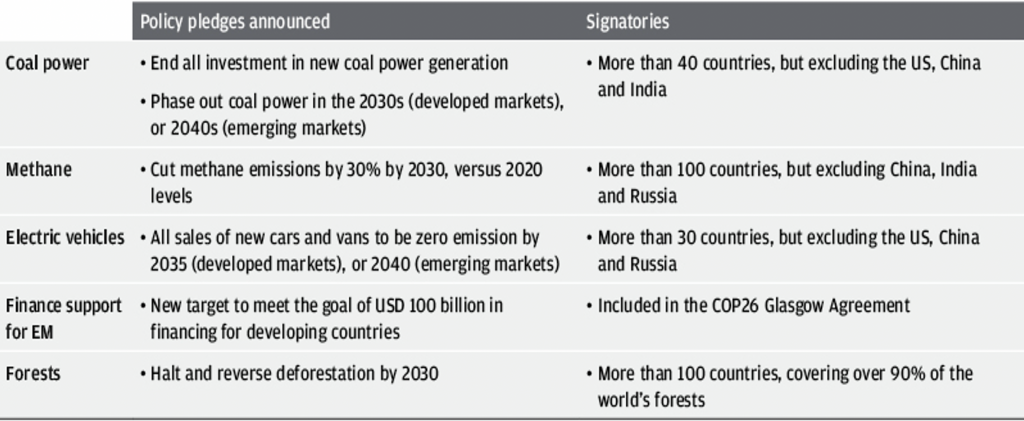

Cop 26… should we be pleased?

More about this in the next couple of weeks but as the Conference has just finished, I thought I’d share with you what was agreed as opposed to what wasn’t.

Source: UKCOP26.org, J.P. Morgan Asset Management. Data as of 12 November 2021.

Question is, I suppose, will they deliver?

ESG investments still favoured

As reported in Investment Week, ESG (Environmental and Social Governance) investments attracted over half the amount of new money pouring into European equity indices in October.

Equity Exchange Traded Funds were strongly in favour with investors adding a net €9.7 billion while fixed income inflows fell by nearly €1 billion.

Hardly surprising ahead of COP 26 but further reinforcement of the momentum in this sector.

Have a great weekend,

Best wishes

Gary and the Investment Team

Risk warning

Please Note: This communication should not be read as giving specific advice regarding your personal circumstances. This would only be given following detailed assessment of your individual needs. The value of investments may fall as well as rise; you may get back less than invested. Past performance is not necessarily a guide to future returns.