What a quarter! A cup of strong coffee and 20 mins of your time is required to assimilate what is going on across global investment markets.

There were some minor tremors as we approached December, but equity markets recovered well as the month progressed. Then January came and it was brutal.

There have been some winners but lots of losers, with strong companies sold indiscriminately on the back of changes, or expected changes, in monetary policy due to the prospects of even higher inflation. Add in the Russian/Ukraine conflict and you have in many ways, a perfect storm.

We have spoken about value versus growth on many occasions and there is no doubt that institutional investors and traders have rotated away from growth and are focusing on more traditional value stocks or companies which are deemed cheap. Of course, they are often cheap for a reason, but we also appreciate that some sectors are likely to fare better than others in a higher inflationary period and as the global recovery gathers momentum.

At Blue Sky, we are particularly focused on thematic investing but undoubtedly, geography will play a big part this year with Europe, China and the Pacific expected to attract a lot of interest.

The FTSE 100, for so long a laggard on the global stage, has proved to be relatively resilient in recent times and, over the last year, has risen strongly. No wonder, with a concentration of energy, financials and commodities in the index. The word here is concentration and, of course, there are times when holding such assets is not good news. It’s also important not to perceive the FTSE 100 as a barometer of the UK economy. It’s certainly not the case, otherwise we would be enjoying a bumper time right now and the outlook for GDP would not be one of weakness!

Supporting the recovery from the early stages of Covid-19 was a consumer boom. Many people had more disposal income but to all intents and purposes, this boom is over as energy prices, supply chain difficulties and rising interest rates dampen the enthusiasm for discretionary spending, certainly in the short-term. However, the travel industry is likely to be a beneficiary with so much pent-up demand.

Whilst the consumer boom may be muted now, we are seeing the early signs of a boom in business spending. Most businesses had to be prudent in the heart of the pandemic and those with good balance sheets used the crises as an opportunity to reposition themselves, become nimbler, and better prepare themselves for future growth. As the global economy responds we expect this growth to become very evident and business spending to increase.

Tech Wreck

I think a recent article in the FT summed up what’s going on, but regular readers will know that we have communicated these changing dynamics, week on week, with the help of LGT Vestra and Legal & General Investment Management (LGIM).

The FT article highlights the tech sell-off but, in particular, the speed in which this market weakened. Technology stocks have been under pressure since last year when rising fears over central banks reversing their stimulative policies triggered ructions across financial markets. Central banks led by the US Federal Reserve (FED) have reinforced their resolve to raise interest rates and this has triggered a broader sell-off.

“The main source of the volatility is the Fed, which is flogging the equity markets with the prospect of tighter monetary policy” said Ed Yardeni of Yardeni Research.

He continued; “The Fed is making a tough transition from easy to tight monetary policy more painful and possibly more prolonged than it has to be. We reckon the beatings will continue until morale improves”.

The gloom has hit some of the industry’s biggest names. Tom Slater’s £15.2 billion Scottish Mortgage Trust has slumped 21% in 2022, its worst stretch of returns since the financial crisis in 2008.

Stock markets last week started to regain their footing after a turbulent January, until that is Meta reported disappointing numbers on the Wednesday evening. The reaction was to wipe more than $230 billion from its market value and triggered another bout of turbulence for many tech stocks. This helped send the Nasdaq Composite index down 3.7% on the Thursday and pushed this year’s losses to almost 10% despite the recovery the day after. The encouraging news is that the Nasdaq and the broader S&P 500 index in the US, is beginning to attract investors back again at these lower levels. This Wednesday (9th Feb), the S&P 500 rose by 1.45% and the Nasdaq by just over 2%.

The “tech wreck” has not been uniform, with companies such as Apple, Microsoft, and more recently Amazon, reporting better than expected results that helped lift their shares.

LGIM also spoke about Meta’s results last week, which is a reminder of what they call the concentration conundrum whereby a single stock was effectively able to pull S&P 500 futures down by nearly -1%.

LGIM’s Views on Tech

The earnings season has not changed LGIM’s view of Tech’s secular growth advantage, beyond the broader economic rebound. Big Tech should have revenue growth of around 15% this year and again next year, beyond which market revenue growth will likely drift back down to mid-single digits. LGIM haven’t seen anything in the earnings season that changes that profile.

The earnings season has not changed LGIM’s view of Tech’s secular growth advantage, beyond the broader economic rebound. Big Tech should have revenue growth of around 15% this year and again next year, beyond which market revenue growth will likely drift back down to mid-single digits. LGIM haven’t seen anything in the earnings season that changes that profile.

Big Tech is increasing cash returns to shareholders. Meta is buying back stock at twice the expected rate. Alphabet is a similar story. Huge acquisitions that move the needle have become difficult because of size and the regulatory backdrop, so companies are increasing capital expenditure (capex) and buybacks instead. This will be a gradual tailwind going forward.

One thing LGIM are none the wiser about is sentiment. A lot of the biggest ‘sell-offs’ have been in Tech (e.g. Netflix, Paypal, Meta). But some of the biggest rallies after results, have also been in Tech (e.g. Amazon, Snap and Alphabet). A muddled sentiment picture, but certainly not one of extreme pessimism. Despite being bashed about a bit through the beginning of 2022, LGIM are sticking to our constructive outlook for the sector.

Temporary Indigestion

We have quoted LGIM on quite a few occasions already but no apologies here as I believe they have encapsulated what has been happening recently. Interestingly, these views are largely shared by our other strategic investment managers, LGT Vestra particularly.

We have quoted LGIM on quite a few occasions already but no apologies here as I believe they have encapsulated what has been happening recently. Interestingly, these views are largely shared by our other strategic investment managers, LGT Vestra particularly.

We have seen some big moves recently, like yields on government bonds up 35 basis points and equities dropping 10% and rallying back 5% in 3 days. Taking a step back from the day-to-day noise, LGIM have taken stock on their overall investment strategy outlook and economic thinking.

- Inflation has continued to surprise beyond their consensus forecasts. An easing of supply disruptions is expected to unfold through the year, but there is considerable uncertainty around how quickly this occurs and at the margin, this appears to be happening more slowly than previously hoped. Central Banks face a dilemma.

- The future growth and inflation mix appears worse than Central Banks had expected too. This has led to a decisively ‘hawkish’ shift without any corresponding upgrade to the growth outlook. The rise in inflation could reflect a one-off adjustment to reopening from the pandemic and the previous deflationary forces could reassert themselves.

- Historically, stocks have peaked about six months before the onset of a recession, but LGIM don’t think we are anywhere near that yet. Aside from the brief, but violent 1987 stock market crash, during the past 50 years, the S&P 500 has never fallen by more than 20% outside of a recessionary environment. Though the current correction is, in LGIM’s view, mainly due to the increased pricing of rate hikes by Central Banks, they believe that equities usually digest higher bond yields well, given time.

- Temporary indigestion can happen if rates increase quickly. This is what has happened in the past weeks. However, the moves by central banks now mean that this has fed into markets with many stocks fairly priced, and LGIM have started to debate whether or not too much has been priced in.

All of this means LGIM will stick with their medium-term position in their multi asset portfolios and are looking for signals to buy more tactical risk on corrections.

Interest Rates and Inflation

In the UK, the Monetary Policy Committee (MPC) surprised most with its hawkish vote. Digging into the details reveals two key reasons why:

- Further evidence of wage-price spiral dynamics developing. First, businesses said they were increasing pay settlements by almost 5% in 2022. This compares with a range of 2-3% in the pre-COVID decade.

- Second, more companies said they were passing on higher labour costs.

A surge in energy costs should, in theory, make consumers poorer and energy producers richer. If workers resist that squeeze in living standards and demand higher pay, the burden then shifts to their employers as profit margins are squeezed. But if companies then pass on higher labour costs and non-energy bills rise, we have a potential wage-price spiral. The MPC sees two-sided risks. At some point, energy prices should fall. But if labour costs have risen in the meantime, services inflation will be higher.

The MPC is acting forcefully to reinforce its inflation-fighting credibility. They reiterated LGIM’s view that the UK household sector is less sensitive to rate hikes than before given more fixed-rate mortgages. It’s unclear when and where rates will ultimately peak, but into next year, household utility bills should fall, pushing inflation sharply down.

Given that there have been some big moves recently, like yields up 35 basis points, equities dropping 10% and rallying back 5% in three days, LGIM have updated their Investment Strategy Outlook and economic thinking.

Despite the repricing of near-term Fed action, there has been only a small change in the market expectations as to where rates will peak over the next few years and this is still below 2%, which is well below the levels ultimately needed to bring inflation back to target.

Alternative Assets

At Blue Sky, we hesitate to call Sustainable assets ‘alternatives’ as they are fast becoming front and centre in the investment world, but we are going to include them alongside infrastructure because they are closely linked.

Many businesses in these asset classes are youthful although there are some huge companies embracing this new paradigm. Rising interest rates have dampened short-term enthusiasm as it is deemed likely to have a detrimental impact on profitability. However, the avalanche of money pouring into these sectors cannot be ignored.

As regular readers know, we have strongly favoured Foresight as an investment provider, mainly because they invest in physical assets and not companies that just participate in this space. Although inflation and interest rate rises have had a negative impact on sentiment there is a flip side. Foresight’s Global ‘Real’ Infrastructure fund aims to deliver an annual return of 3% plus inflation. Foresight’s recent comment from one of their fund managers, was that this dynamic will help support performance once it feeds through.

As regular readers know, we have strongly favoured Foresight as an investment provider, mainly because they invest in physical assets and not companies that just participate in this space. Although inflation and interest rate rises have had a negative impact on sentiment there is a flip side. Foresight’s Global ‘Real’ Infrastructure fund aims to deliver an annual return of 3% plus inflation. Foresight’s recent comment from one of their fund managers, was that this dynamic will help support performance once it feeds through.

Ukraine/Russian Conflict

Besides Boris, this conflict now appears to dominate our news feeds. Of course, its worrying and we must watch this space very closely. Some of the angst is already in the price of assets. I like the context from LGT Vestra recently:

“With all that’s happened over the past three years, it’s hard to believe that we are staring down the barrel of the largest concentration of military force in Europe since the Cold War. Despite bolstering defences on the border and the extraction of diplomats in a political display of concern, the threat of war is far from certain. Russian President, Vladimir Putin, comes from a political culture very unlike ours in the West, where negotiations often start with threats rather than attempts at understanding. While interpreting the next move of Mr Putin has been compared to ‘reading tea leaves’, the potential impact on markets is fortunately rather more predictable”.

Energy Prices

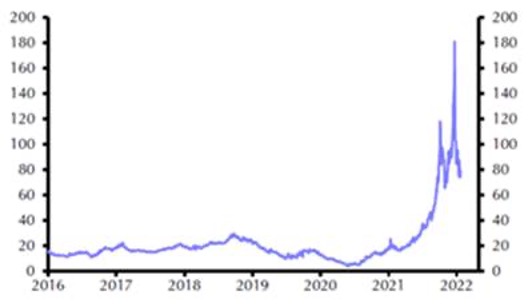

One significant and more obvious implication would be the effect on already volatile energy prices. Russia is the lead supplier of natural gas, accounting for about 24% of the world’s total reserves. Natural gas prices are now five times their average price during 2016 to 2020 (see chart below), and in the event of conflict we could see spikes back to their astonishing peak at the end of last year, particularly given that gas stocks are already low in major European countries.

Natural gas price (€ per Mwh)

Source: Capital Economics

Economic Recovery

Higher energy prices have a negative effect on household and corporate real incomes, and the fear for investors remains that further disruption will slow economic recovery. However, in this case, it is doubtful that any rise in in gas price could compare to the vagaries of the pandemic, especially with the current growth in employment and the level of excess savings. Furthermore, it is highly likely that governments would be forced to run larger deficits in order to compensate households for higher energy bills and enable recovery to continue.

It is likely that the effect on inflation will be short lived. If gas prices reached their peak of €180 and stayed there, inflation would rise by around 1.5%, assuming that the cost was fully passed through to households. But then it would drop back sharply, and the impact on household incomes would strengthen the case for the European Central Bank (ECB) to keep policy looser.

Recent History

While the situation may have escalated, we must remind ourselves of recent history and what to expect. The most relevant comparison is 2014 when Russia invaded Crimea and, as the chart below shows, European equities held up quite well even as Russian equities took a nose-dive.

European equities over the course of 2014

Source: Refinitiv

If one side makes a miscalculation, a full-scale conflict cannot be overlooked. However, history, and common sense, all suggest that a peaceful compromise is in the rational interests of the key players.

Obviously, the economic fallout from a conflict would depend on the extent and duration of any action, but LGTV and we at Blue Sky, are closely monitoring the situation and have limited direct exposure to asset classes that would be most at risk.

What about China?

Whilst on the subject of more extreme governments, we mustn’t overlook China; the world’s second largest economy.

The winter Olympics (unbelievably, I haven’t watched any yet) may well dominate thoughts around China and, of course, the Chinese are determined to put on a real show of strength and optimism.

China has had it tough and certain provinces have been shut down with a zero tolerance to the virus. This certainly hasn’t helped China’s economy, but it’s also had an adverse impact on supply chains around the world, serving to elevate prices and bolster rising inflation numbers.

The government has stepped in to help the economy and has reduced interest rates slightly with a cut of 0.1% to 2.85%, the first reduction since April 2020 – at odds with what is happening across the developed economies. China’s Central Bank cut the reserve requirement ratio for agriculture and Small and Medium Enterprise (SME) lending programmes. It is anticipated more easing measures are to come.

Blue Sky, along with our investment partners, see this as an attractive area for investment, although we prefer a broader exposure across the Far East region.

LGT Vestra commented that “they see potential opportunities in China and elsewhere in Asia, with the latest easing supporting broader financial conditions. The risk of political interference is always present, but valuations have adjusted to consider this”.

Essence from our Strategic Investment Houses

LGT Vestra are using the sell-off to top up holdings that they think have been oversold. JPMorgan, a new addition as one of our core strategists, are similarly adding to positions. Their broad conclusion is that solid data is in line with their upside scenarios. They like financials, utilities, information technology, communications services and healthcare. They also still like the consumer discretionary spending sectors, despite rising inflation, as they believe companies will benefit as the global economy gathers pace.

Geography wise, LGIM like Europe and Asia, as do we at Blue Sky. The recent switch resonated with these dynamics. They have been looking to reduce their mid and smaller cap UK holdings as the UK is expected to encounter exaggerated supply chains issues via Europe.

In common with both companies, is their commitment to sustainable investments. Foresight also has sustainability at the heart of everything they do. They reiterated that although their assets are sensitive to inflation and changes in monetary policy, they are invested in physical assets which offer long-term inflation protection. Undoubtedly, they have been hit by the fall out in sustainable stocks as well which has exaggerated short-term performance. It’s important to remember that most of the contracts are long-term and with governments paying the bills, along with the inflation linked approach, this asset class is important as a diversifier.

Latest News

- UK GDP rose in 2021 by the highest rate since 1940

This is despite Delta and Omicron in 2021. The increase followed a record 9.4% decline in 2020.

- Encouraging news from the CBI

The latest January Confederation of British Industry (CBI) trends survey showed that investment intentions over the next year rose to their peak level since 1988 while order books are running at close to their highest level since the data began in 1977.

- ECB reinforce their relaxed monetary policy

As reported in Bloomberg only this morning, the ECB (European Central Bank) are keen not to act too hastily in tightening the monetary policy reins. The feeling is that if they react too quickly, they may jeopardise the recovery of economies. - Equities fall Thursday/Friday due to rising US consumer price increases

US consumer prices climbed 7.5% in the year to January, the latest inflation report on Thursday showed. This has prompted speculation that the Federal Reserve may rapidly raise borrowing costs.

Summary

Well, no wonder I haven’t watched the Olympics with all this going on! Worse still, I’m an Everton fan and have also been watching Weymouth FC become marooned in the bottom three of the National league (my youngest boy is in the 1st team squad, but can’t be blamed, as he hasn’t made an appearance from the bench yet!).

Looking forward, I’m hoping and expecting a better month on all fronts!

Have a great weekend.

Gary and the Blue Sky Team

Risk warning

Please Note: This communication should not be read as giving specific advice regarding your personal circumstances. This would only be given following detailed assessment of your individual needs. The value of investments may fall as well as rise; you may get back less than invested. Past performance is not necessarily a guide to future returns.